Indian Holcaust My Father`s Life and Time, Chapter: Nine Hundred Twenty Three

Palash Biswas

Mobile: 919903717833

Skype ID: palash.biswas44

Email: palashbiswaskl@gmail.com

India's economic growth is expected to slow to around 6%, dragged by domestic issues, but the government is focused on getting the country back on a growth path, Prime Minister Manmohan Singh said.

"Our exports have shrunk and the fiscal deficit has gone up on account of a variety of factors," Mr. Singh said in a speech at an awards ceremony in Mumbai late Saturday.

Prime Minister Manmohan Singh, who has been concerned over the atmosphere of perceived gloom over last several months, today utilised the occasion of Diwali to express hope that a "new phase of optimism" will dawn on countrymen. Singh, whose government has been battling a number of corruption allegations and attack over economic decisions like FDI in retail, has been maintaining that "mindless atmosphere of negativity and pessimism" would hurt the country, particularly the investment prospects. On Saturday, he said his government had dispelled the atmosphere of 'gloom and doom'.

Happy Diwali Mango Men!The Banana republic gifts you inflation and a destroyed production system. The Corporate raj promises new recipe next of growth agenda!Assocham sets 15-point agenda for parties fighting polls in Gujarat. India incs, thus , formally, presses for political return for the donation paid. Get ready for serious infections ahead.For industry, strong social safety nets require revenue generation for the exchequer, and this can happen only with high, steady and sustainable growth. At this juncture, this requires a strong investment revival. The government has announced a series of measures which has improved sentiment, but supporting policy measures are needed now. Another disturbing trend over the past few years, together with slowing capex, is a drop in productivity of capital (known as Incremental Capital Output Ratio).One manifestation of the latter is slippage in India's rank in the 2013 Global Competitiveness Index (GCI) to 59 (of 144 countries) from 56, the year before. Clearly, the focus must be on both increasing investment and improving productivity.On the other hand,confidence in the state of the world economy has improved to some extent but majority of experts from business, government and civil society are still pessimistic, says a survey by World Economic Forum.The world is changing fast with a number of challenges facing the mankind that needs to be tackled in order to sustain economic growth worldwide, officials at a global conference in Dubai warned political, economic and social thinkers to prepare the mankind better to face those challenges.Meanwhile,the government today received bids worth more than Rs 9,200 crore on the opening day of auction for 2G mobile phone spectrum that drew scant interest due to high base price.The much-awaited auction for 2G spectrum that was freed following the cancellation of 122 telecom licences started at 0900 hrs on Monday. The government expects to raise around Rs. 40,000 crore through the auction.

Scaling tow ards a new high, gold continued its upward march for the seventh consecutive day on Monday in Mumbai's Zaveri Bazaar.Investors lapped up 'paper gold' at a special trading session at bourses on Sunday which coincided with Dhanteras that marks the beginning of the three-day Diwali festival.

Dear Mango Men! Get ready for the final assault, the monopolistic aggression to get hold of your land, home, livelihood, water bodies, forest, environment, citizenship,identity , civic and human rights. The Prime Minister is too busy to manage the required numbers to get the anti people financial bills passed in the winter session of the Parliament and push forward for various anti people measures branded as reforms to continue the growth story of exclusion, excommunication and ethnic cleansing!

In a bid to demonstrate that various arms of the government are on the same page when it comes to approvals, which have slowed down mega projects, Planning Commission deputy chairman Montek Singh Ahluwalia has said that most ministries are now largely in support of creating a National Investment Board (NIB).

The government is likely to soon decide on setting up NIB, which is designed as an overarching mechanism that will help it move ahead on projects and investment proposals by resolving inter-ministerial conflict.

"We had taken the view that there is something seriously wrong in the way we process approvals because nobody is taking a holistic view, nobody is saying this is a good project... How do we solve these problems? What we said was we need a kind of an overarching mechanism. The finance minister then suggested a specific way of doing it... which I am certainly strongly supporting," Ahluwalia told a gathering of the who's who of Indian business during a panel discussion on Agenda for Reforms at the Economic Times Awards for Corporate Excellence 2012.

The Indian economy will be fastest growing over the next 50 years, leaving behind populous neighbour China, but may still rank towards the bottom of the heap in terms of living standards of its common citizens measured by per capita income, according to Paris-based Organisation of Economic Cooperation and Development (OECD).

Domestic infrastructure companies should be allowed to list in overseas capital markets through direct equity shares in a bid to access low-cost funds in order to spur growth, industry body Assocham has suggested to the government."Listed and unlisted domestic infrastructure companies be allowed to list in overseas capital markets through direct equity shares as companies once listed abroad have better access to low cost funds and simultaneously they may also be allowed to set up an entity abroad to raise equity and invest the same in India," it said in a letter to Finance Minister.Also, the transfer of holding to such an overseas entity from an Indian entity should be permitted at erstwhile book value, prevalent till March 31, 2010, as infrastructure projects are long-term and require high gestation, it said.

Expressing disappointment over poor show by industrial production in September, India Inc on Tuesday pressed for rate cut by the RBI to boost production and further revive the economic growth.India's industrial output unexpectedly shrank in September and its trade deficit expanded to the widest in several years in October, indicating that the worst for the economy isn't over and measures including monetary easing may be needed to revive growth. Industrial output contracted 0.4% from a year earlier in September, hurt by the poor performance of the manufacturing sector, government data showed Monday. The government also downwardly revised the output reading for August to a 2.3% expansion from 2.7% reported previously. Stocks turned negative and the rupee fell to its lowest level in two months against the U.S. dollar. The Bombay Stock Exchange's Sensitive Index was down 0.1% at 18661.72 in afternoon trade, while the dollar was at 55.11 rupees, compared with 54.75 rupees late Friday. Factory output has shrunk in five of the seven months through September as high interest rates eat into demand and slow policy reforms hurt investor confidence. Economic growth in India has slowed to its weakest in nearly a decade.India's trade gap rose to $20.96 billion from $18.08 billion in September as the country's heavy dependence on imports to meet its oil needs pushed up overall imports, while weak demand in the U.S. and Europe led to a decline in exports.

India's September industrial production data released Monday showed an unexpected contraction of 0.37%. What is even worse is that the August growth rate was also revised downward by 0.37 percentage point to 2.29% from 2.66%.

This data is a big jolt since India's festival period has been in full swing and this generally tends to boost production as inventories are built up.

What is even more worrying is that the index value itself has been falling since March (with the exception of May), indicating that the worse may not yet be over of the economy.

Even if one accounts for the notorious volatility of production data, the downward trend — which indicates consumer fatigue — is clearly visible.

In fact, both the three-month and the six-month moving average exhibit this weakening trend. From April to September, the first six months of the current financial year, India's industrial production remained virtually stagnant (it grew by 0.1%) as compared to the same period in the previous year, when it grew 5.1%.

Faced with a dramatic slowdown in the economy—the pace of growth is the slowest in nearly a decade—and warnings from ratings firms that the country needs to quickly boost capital inflows and narrow its fiscal deficit, New Delhi has taken several steps since mid-September to allow for more foreign investment. It is attempting to slash government subsidies on diesel to rein in the budget gap.

The government has laid out a fiscal deficit road map, planning to bring the deficit down to 5.3% of gross domestic product this year, and to 3.0% by 2016-17. The fiscal deficit was 5.8% of GDP in the last fiscal year, when growth slowed to 6.5%, compared with over 8.0% growth in the recent past.

Investors have applauded the government's recent moves, which amount to some of the most significant reforms since India started opening its economy in 1991. However, the steps, which include clearance for foreign investment in multibrand retail, face execution risks due to intense political opposition from both within and outside of the coalition government.

Measures such as those allowing for higher foreign investment in the insurance sector as well as measures allowing foreign funds in the pension sector for the first time need to be approved by parliament, which Mr. Singh hopes will happen as soon as possible.

Seeking to send out a strong message that the Centre is committed to action, the panel — comprising commerce and industry minister Anand Sharma, telecom minister Kapil Sibal, Unique Identification Authority of India chairman Nandan Nilekani and Ahluwalia — sought to highlight how the government is moving full steam ahead in making investments happen.

Ahluwalia said some ministries have strongly supported the proposal while only one or two have opposed it. "My hope is that it will come to the cabinet soon. Soon means a week, maybe two weeks and I do think that we should definitely do it. The balance of opinion among all the cabinet ministers is that it should be done."

Putting his weight behind the creation of NIB, Sharma said that the government is uncomfortable with the recent World Bank report which talks of time delays in India and relative ease of doing business in other emerging markets. "You have a minimum of 15 million people joining the workforce every year and, therefore, we need to create an environment where job creation takes place."

Responding to a question from HDFC chairman Deepak Parekh, the panel members made it clear that they were at work on reforms. Instead, Sibal sought to blame the judiciary, the media, the opposition and the CAG for the policy paralysis in the past. "The paralysis occurred because of three factors: one, the erudition of the CAG; two, the media; and three, the court. It is the symbiotic relationship between these three institutions that has resulted in a situation that we find difficult to deal with on a daily basis and yet the government continues to take decisions," Sibal said.

Besides the creation of NIB, growth and investment dominated the conversation with the panel members agreeing that the Centre was taking quick decisions to revive growth to over 8%. They also highlighted that the government is focusing on the youth and has identified foreign direct investment, digital connectivity and everywhere banking as key themes to reach out to them. Inclusive growth, the panel members said, was their mantra and would push ahead with reforms more vigorously even as they made a case for the industry to set aside a part of its profits for skills development.

"You have 650 million people in this country who are less than 25, that is half the population of this country. We need to look at India through the eyes of our children and what our children want is instant connectivity, what our children want is digitization, what our children want is instant relief and that can only come about if we transform our economy and connect with the digital world. We must connect with 250,000 villages of this country through technology," said Sibal.

Speaking about Aadhaar, a pet project of the government being championed by Nilekani, the UIDAI chief said it was the largest social inclusion programme which already covered 250 million people and a three-phase plan for direct cash transfers using Aadhar-enabled accounts was in progress. "It will help in reducing wastage in subsidies that will in turn contribute to (controlling) fiscal deficit. The fact that it is going to be an automated system which allows people to get their money from any location will help in dramatically reducing retail corruption," said Nilekani.

India's Prime Minister Manmohan Singh has pledged to follow up his recent burst of economic reforms with further measures to restart stalled infrastructure projects, attract foreign investment and reverse the slowdown in Asia's third-largest economy.(Source: Ft.com)

"Some people still try to make FDI into a bogey, even invoking fears of the East India Company," Mr Singh said, a reference to the British corporation which governed large parts of India for around a century until 1858.

"Our efforts to raise the investment rate will mean higher imports. FDI is perhaps the best source of external financing to finance the deficit," he said.

After a period of chronic inaction, investors have been heartened by recent announcements by Mr Singh and his newly appointed finance minister Palaniappan Chidambaram, moving to allow greater foreign investment in sectors including airlines, retail and pensions.

India's economy is projected to expand by around 5.5 per cent in the next financial year, although Mr Singh says the country can return to average growth above 8 percent over the next five years, if further reforms are introduced.

Infrastructure would be one area of priority, with government planning $1tn in fresh spending, including what the prime minister described as a range of "iconic projects", such as elevated rail lines in the financial capital Mumbai, alongside two ports and eight airport developments.

However many analysts remain sceptical, seeing scant evidence that the world's largest democracy can deliver the legislative changes needed to underpin some proposed reforms, including opening up the insurance and banking sectors, given India's fractious and divided parliament.

Equally a history of delays to major projects, including power stations and steel plants, lead many to doubt that the country is capable of delivering the type of large-scale schemes common in other Asian emerging markets, notably China.

"If you look at why India's growth has slowed, it is not a mystery" says Gita Gopinath, an economist at Harvard University, speaking at the annual meeting of the World Economic Forum business group in New Delhi last week.

"Reforms have happened only on a spasmodic basis . . . India's people, and its government, must realise that these things need to happen on an ongoing basis every year, not just once every thirty years."

Investors are awaiting the results of two government reviews re-examining heavily criticised tax changes, including those designed retrospectively to recoup at least $2.6bn of tax from UK-based telecoms company Vodafone. Both are due to report in the coming weeks.

Business groups are also watching carefully for action to unblock dozens of stalled infrastructure projects and increase coal imports to the country's fuel-starved power plants, with senior officials promising progress on both fronts by the end of the year.

Even so, around half of the slated infrastructure spending increases are set to come from India's battered private sector, just at the moment when major industrial conglomerates have cut investment sharply, against a backdrop of slowing demand and high interest rates.

A number of well-known business leaders, including estranged billionaire brothers Anil and Mukesh Ambani of the Reliance group, have also been targeted by anti-corruption campaigners in recent days. Both brothers deny any wrongdoing.

Even so, analysts say even modest reforms could help to bolster investment sentiment further, potentially persuading these business leaders to begin investing again, especially if interest rates are trimmed early next year.

"Growth falling to around 5 per cent is like zero growth in a more developed economy, given the demographics and the need to create jobs here," says Ajit Ranade, chief economist of the Aditya Birla Group, one of India's largest conglomerates.

"But even if they can't find any really big ticket items, they should go through their closet and dust down the long list of smaller things that don't parliamentary approval, all of which boosts sentiment and helps to bring in more foreign investment."

Speaking over the weekend, Mr Singh defended plans to attract capital from abroad, while admitting that India's precarious public finances now required more international money to plug a growing gap between what the country imports and exports.

Mr. Singh admitted that delays in a large number of infrastructure projects due to late clearances have played a part in the overall slowdown.

"In the power sector, fuel supply has been a problem. In fact, the pricing system across the entire chain in the power sector needs to be rationalized," he said, adding that New Delhi is trying to resolve the situation by ramping up coal production and promoting pooling of imported coal.

"Investment in infrastructure has to be in the vanguard of public investment for many years to come and we are working in that direction," he said.

Experts estimate that problems associated with India's infrastructure-—including roads, ports and airports—shave off about two percentage points from its gross domestic product growth annually, making a speedy overhaul of power infrastructure crucial to boosting economic growth.

The government is expected to decide on setting up a National Investment Board, aimed at providing one-stop clearance for large infrastructure projects, within the next two to three weeks, the government said late last week.

According to the plan, the board would provide clearance for infrastructure projects of $200 million and above to avoid delays due to bureaucratic hurdles and multiplicity of authorities involved.

The prime minister also backed the Reserve Bank of India's decision not to lower key lending rates despite the finance ministry and the industry seeking a rate cut to boost growth. The Reserve Bank of India stood pat on rates to keep stubbornly high inflation in check.

"We must recognize that lower inflation is good both for growth and for making growth more socially inclusive," Mr. Singh said.

India is also making efforts to correct the negative perception about the country among investors due to two recent tax policies—the General Anti Avoidance Rules and a retrospective law amendment to tax foreign deals involving local assets, Mr. Singh said.

The measures, proposed in March, had hurt capital inflows, forcing the government to postpone the implementation of the GAAR by a year and to set up a panel of experts to review both policies.

"We hope to announce decisions on all of these issues within the next few weeks," Mr. Singh said.

Prime Minister Manmohan Singh continued to reach out to important allies, the Samajwadi Party and the Bahujan Samaj Party. On Sunday BSP chief Mayawati and senior party leader Satish Mishra were invited for lunch at his residence in New Delhi. On Friday night, his guest was SP's Mulayam Singh Yadav and his son, Uttar Pradesh chief minister Akhilesh Yadav.

The meetings, the first such after Mamata Banerjee of the Trinamool Congress withdrew support to the UPA government, is in preparation for the winter session of Parliament, where, the government fears, Banerjee could move a no-trust motion or at least a combined opposition resolution in the Lok Sabha against FDI in multi-brand retail.

With over 400 CEOs in attendance at the ET Awards for Corporate Excellence, Prime Minister Manmohan Singh, the original architect of reforms, spoke clearly and boldly about the need to keep pushing ahead on this road. Here is the full text of his speech:

http://economictimes.indiatimes.com/news/news-by-company/corporate-trends/et-awards-2012-we-can-make-a-difference-to-the-world-if-we-do-the-right-things-says-pm-manmohan-singh/articleshow/17187066.cms

I am delighted to be here for the Economic Times Awards for Corporate Excellence. This annual event provides a valuable opportunity to appreciate some dynamic and creative entrepreneurs for their outstanding contributions.

Growth in statistical terms is meaningless unless it helps every individual and all sections of society, which is where the trickle-down theory has its genesis. If we have been able to withstand the pressure of the global meltdown, it is because of our resilience and our unique approach to the problem. It was not borrowed or taken from an eminent economist's textbook. We adopted what we considered best suited to our country, society and culture. I congratulate all the winners of the Awards, and hope that they inspire others to be equally innovative and productive.

Six years ago, I was here in Mumbai at an ET Awards function that celebrated 15 years of reforms. The economy was booming and the mood was exuberant. Double-digit growth seemed eminently achievable. Foreign Direct Investment ( FDI) and Foreign Institutional Investment (FII) flows were rising rapidly. Government revenues were buoyant and the fiscal deficit was shrinking. The sense of optimism was an all pervading one.

GLOBAL STORM

Times have changed since then. The global economy is under stress. Growth rates have slowed down everywhere. There is considerable uncertainty about the period over which growth will revive in the industrialised world.

The Indian economy has been affected by these developments. Our exports have shrunk and the fiscal deficit has gone up. Growth decelerated to 6.5% last year and may be only around 6% in the current year. This has dampened investor sentiment. Doubts are being raised in some quarters about the India growth story going astray.

Economies go through ups and downs and downturns do dampen spirits. However, such downturns can have value if they make us focus on the weaknesses that are masked when times are good. India's slowdown is partly because of the global downturn, but it is partly also because of domestic constraints which have arisen.

We cannot do much about the global slowdown. Though we can certainly make a difference to the world if we do the right things at home to accelerate our own growth. But we can, and we must, correct our own weaknesses, and create new opportunities for economic growth and employment at home. This is the challenge before us. I assure you, this will now remain the focus of our policy in the months ahead.

In recent weeks the Government has taken several steps with these objectives in mind. Our objectives have been the following:

(a) Stabilise government finances and make fiscal deficit manageable, so that higher growth is possible and sustainable;

(b) To make this growth process socially and regionally inclusive and equitable. The key pillars of inclusive growth are new employment opportunities and lower inflation;

(c) To step up public investment as well as public-private partnerships, especially in infrastructure;

(d) To tap into available capital and technology from around the world that seeks investment opportunities in India.

Industry chamber CII said the Reserve Bank should intervene and cut interest rates. The RBI needs to reduce repo rate (short-term lending rate) by 0.5 per cent and Cash Reserve Ratio (the portion of deposits banks are required to keep with RBI) by 0.5 per cent.

"While fully appreciating the imperative of anchoring inflation, it is our view that RBI now needs to intervene and reduce interest rates, since a complete sacrifice of growth is not in the interest of the economy," CII Director General Chandrajit Banerjee said.

Sharing similar views, Ficci President R V Kanoria said, it hopes RBI will relook at its monetary policy in the light of latest Index of Industrial Production (IIP) figures and reduce interest rates.

Assocham Secretary General D S Rawat also said that the RBI needs to take a constructive view while announcing the next credit policy.

The RBI has refrained from cutting interest rate fearing that it could fuel inflation. The central bank is scheduled to come out with next mid-quarter policy on December 18.

Industrial production contracted by 0.4 per cent in September on account of dismal performance by manufacturing and capital goods sectors.

The industrial output growth rate turned negative in September after showing 2.3 per cent growth in the previous month. The IIP was 2.5 per cent in corresponding month last year.

The country's economic growth rate during the first quarter of the current fiscal was 5.5 per cent.

Recently, RBI in its half yearly review of the monetary policy had sharply lowered this fiscal's economic growth projection to 5.8 per cent, from 6.5 per cent estimated earlier. This was done in the view of global and domestic factors like poor investments and subdued demand.

Further, Assocham said, the continued negative growth of the manufacturing sector has got wider implications and needs to be addressed on a priority basis.

The IIP data suggests that output of manufacturing sector, which constitutes over 75 per cent of the index, contracted by 1.5 per cent in September, as against a growth of 3.1 per cent in the same month last year.

Calling for faster implementation of pending reforms like GST, Ficci said at this juncture, it is important that the government does not lose momentum on reforms front.

Besides, Assocham said it has been urging the policy makers to announce special incentives for investors in manufacturing capacities and improving credit availability, among other things.

Assocham president Rajkumar Dhoot said, "Lack of availability of sufficient long term debt, dearth of equity funds, withdrawal of tax sops and absence of quick decision making are the key reasons responsible for a sluggish infrastructure growth in India."

Advocating the need for long-term bank finance availability for the sector, the industry body has suggested for mandatorily increasing the bank lending by way of incentives.

"Considering the priority status to the infra sector, a certain percentage of exposure should be made mandatory for all the banks just on the lines of export financing," it said.

"Besides, obligatory targets should also be imposed upon private sector banks and foreign banks operating in India as currently, major portion of infrastructure lending is contributed by public sector banks."

It suggested that banks may be permitted to issue long-term, tax free bonds for the purpose of lending to infrastructure sector at a lower rate of interest.

Provisions may also be made by the Reserve Bank of India (RBI) to provide interest subsidies to the banks for their exposure in this sector, it said.

Incentives doled out to the infrastructure entrepreneurs earlier, should be restored and current regulations be amended, it added.

Apex industry body Assocham has proposed a 15-point growth agenda to the political parties for inclusion in their election manifestos for the ensuing Gujarat Assembly elections. The body's suggestions aim to create consensus on certain significant economic issues to achieve double digit growth in the next decade.

The chamber has earmarked issues of utmost significance under the headings – agriculture, economics, industry, infrastructure, international trade, politics and services. But Assocham emphasises that parties should create consensus on General Sales Tax (GST).

The paper suggest political parties to include infrastructure development, public private partnership (PPP), cluster-based development approach, agriculture, food processing, power, automobiles, textiles, transport, healthcare, pharmaceuticals, information technology, real estate, special economic zones (SEZs), export promotion zones (EPZs), civil aviation, education, telecommunication, tourism and international trade in their election manifesto.

The paper titled 'ASSOCHAM Suggestions for Election Manifesto of Political Parties in Gujarat,' was jointly released by Bhagyesh Soneji, chairperson, Gujarat Council of The Associated Chambers of Commerce and Industry of India (ASSOCHAM), Jay Ruparel, co-chairperson Gujarat Council and national secretary general, DS Rawat.

"MSME sector is a priority area as it requires low investment, lower technical skills and generates more employment and provides purchasing power in the hands of people at lower strata and has the potential to lift the GSDP level effectively," said Rawat.

India's economic growth is expected to be less than 6% in the next fiscal due to slowdown in western markets like US and Europe, a survey has said. "Majority of respondents surveyed said they expect the country's gross domestic growth in the range of 5-6% next year," said a

survey jointly conducted by industry body Confederation of Indian Industry (CII) and McKinsey & Co.

As many as over 50% respondents said that the euro crisis, followed by slowdown in the US, as well as increasing oil prices, are expected to have the biggest impact on the Indian economy, it said.

The growth rate in the first quarter of this fiscal was 5.5%.

In the budget for 2012-13, then finance minister Pranab Mukherjee had projected the economy to grow by around 7.6%.

Recently, the Reserve Bank of India (RBI), in its half yearly review of the monetary policy, had sharply lowered this fiscal's economic growth projection to 5.8%, from 6.5%, in view of global and domestic factors like poor investments and subdued demand.

CII said that around 32 CFOs from leading Indian companies across sectors including manufacturing, information technology, consultancy and financial services participated in the survey.

The survey added that most respondents felt corruption is also affecting businesses.

Besides, the survey said, the Indian economy's outlook is 'cautiously optimistic' and key enablers to fuel the economic growth include increased FDI, reduced fiscal deficit and enabling corporate growth.

It added that a majority of people surveyed said the General Anti-Avoidance Rules is a step in the wrong direction.

Also, over 80% CFOs said they expect their company's top line growth to be same this year compared to last year, it said.

According to Paris-based Organisation of Economic Cooperation and Development (OECD),during 2011-2060 India's gross domestic product (GDP) - or the total value of all goods and services - would grow at an average of 5.1% a year, among the fastest in the world, compared to China's 4% growth rate during the period.

India's per capita income will also grow more than 7-fold during this period, but the country will still rank towards the bottom by 2060 in absolute terms, said the report titled 'Looking to 2060: Long-term global growth prospects.'

The next 50 years will see major changes in the relative size of world economies.

Fast growth in China and India will make their combined GDP soon surpass that of the world's richest seven economies - called the G7 economies. Notwithstanding fast growth in low-income and emerging countries, large cross-country differences in living standards will persist in 2060, the report said.

"Income per capita in the poorest economies will more than quadruple by 2060, and China and India will experience more than a seven-fold increase, but living standards in these countries and some other emerging countries will still only be one-quarter to 60% of the level in the leading countries in 2060," the report said.

"Income per capita in the poorest economies will more than quadruple by 2060, and China and India will experience more than a seven-fold increase, but living standards in these countries and some other emerging countries will still only be one-quarter to 60% of the level in the leading countries in 2060," OECD said.

"The extent of the catch-up (in terms of living standards) is more pronounced in China reflecting the momentum of particularly strong productivity growth and rising capital intensity over the last decade," it said.

This will bring China 25% above the current income level of the US, while income per capita in India will reach only around half the current US level, it added.

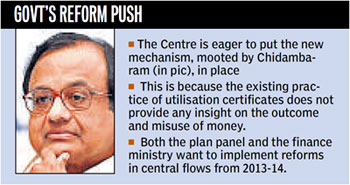

FM's reform push resisted from within

FM's reform push resisted from within

Chetan Chauhan, Hindustan Times

New Delhi, November 12, 2012

http://www.hindustantimes.com/India-news/NewDelhi/FM-s-reform-push-resisted-from-within/Article1-958200.aspx

Finance minister P Chidambaram's grand plan to redefine how the Centre spends its funds through state governments is facing stiff opposition from within, pushing the Planning Commission to seek the cabinet's views on the proposal. The Centre disburses billions of rupees to states for

achieving national developmental goals, but its effective use remains an area of concern. Though the Planning Commission had suggested reforms, Chidambaram — in a letter to Prime Minister Manmohan Singh — sought for more.

The finance minister wants the administration of over 100 central schemes with annual outlay of less than Rs. 300 crore to be transferred to the state governments, so the Centre

can concentrate on 17 big-ticket flagship schemes. He also said that no new scheme in the 12th Five Year Plan (2012-17) of less than Rs. 500 crore should be permitted.

can concentrate on 17 big-ticket flagship schemes. He also said that no new scheme in the 12th Five Year Plan (2012-17) of less than Rs. 500 crore should be permitted.However, the plan panel estimates that his proposal would leave 17 central departments with no central scheme to administer, raising questions on the future of the bureaucracy linked with these schemes.

If the schemes are transferred, many bureaucratic positions in these ministries would have to be dissolved as the central government would be implementing only 73 programmes.

"The implementation of this recommendation will face operational difficulties," the plan panel had said in a note circulated for the consideration of the Union cabinet.

Chidambaram had also proposed a new norm of minimum 25% share in funding for general category states, and 10% for special category states, to utilise central funds.

The proposal is contentious because the Centre, on an average, shared 80% of the funds for flagship schemes, worth Rs. 6,60,000 crore, in the 11th Plan (2007-12). In the case of Right To Education, the government had agreed to pay 90% of the funding requirements.

"Any change will be resisted by the state governments and even the ministries, whose budgets would fall," a senior

plan panel official said, adding that the cabinet has been asked for its view.

8 Nov, 2012, 06.13AM IST, ET Bureau

Agenda for Reforms: Four stories that show how policy shifts have touched individual lives

http://economictimes.indiatimes.com/news/news-by-company/corporate-trends/agenda-for-reforms-four-stories-that-show-how-policy-shifts-have-touched-individual-lives/articleshow/17137787.cmsThe ultimate objective of an economic policy is to make a meaningful and lasting impact on people's lives. Here are four stories, from four diverse spheres, when a radical policy shift initiated by the government in the past few years went on to touch individual lives for good .

Full Coverage: ET Awards for Corporate Excellence 2012

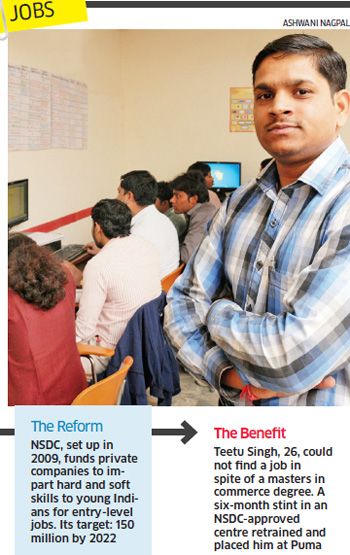

Jobs: Ready To Work:

A skills programme is making the youth job-ready . In throngs and across sectors. And for little or no money.

By Ahona Ghosh

Even after a masters in commerce from Chaudhary Charan Singh University in Meerut, 26-year-old Teetu Singh had no job prospects for months. Until April, when he came across GRAS Academy in Ghaziabad, Uttar Pradesh. GRAS, a vocational training institute , was offering a six-month course in basic accounting. Singh jumped at the chance to brush up his knowledge and at its promise of a job.

Even after a masters in commerce from Chaudhary Charan Singh University in Meerut, 26-year-old Teetu Singh had no job prospects for months. Until April, when he came across GRAS Academy in Ghaziabad, Uttar Pradesh. GRAS, a vocational training institute , was offering a six-month course in basic accounting. Singh jumped at the chance to brush up his knowledge and at its promise of a job.Also Read: Six reasons why the current narrative about graft is wrong

Last month, GRAS made good on its promise and placed Singh as an account executive at a warehouse of sports goods company Puma in Ghaziabad. Millions like Singh have the classroom knowledge and a degree, but are unemployable because they lack specialised and soft skills. A few million join them, year after year, dulling India's 'demographic advantage'.

Best Reads of The Day:

Obama win won't trigger market rally as local issues weigh

Obama's re-election unhealthy for Indian IT: Swaminathan SA Aiyar

Rich buyers making a beeline for disputed properties

'America under Obama can still be a great nation'

But things are changing. The government is putting in place the pieces to train people in throngs in the age group of 18-35 years. Spearheading this effort is the National Skill Development Corporation (NSDC), which the government set up in 2009 to fund private entities—through loans, equity and grants—to impart hard and soft skills to young Indians for entry-level jobs. Its target: make 150 million people job-ready by 2022. "This is a demand-driven model and trainees are mandated by this system to get a job at the end of it," says Dilip Chenoy, MD and CEO of NSDC.

Noida-based GRAS runs 42 centres in North India. It offers entry-level courses in several sectors, including IT, retail, construction and sales, and also imparts soft skills. Companies, too, benefit from this engagement: they get more numbers and better quality. "On an average, we recruit 40% of our employees from NSDC-partner centres," says Ramesh Mitragotri, chief people officer at Aditya Birla Retail-More.

The courses, which are heavily subsidised, are primarily meant to draw candidates from underprivileged backgrounds. Teetu Singh, today, earns Rs 6,000 a month as an account executive. His family of five, including his parents and two younger brothers, were living off his father's meagre salary of Rs 1,400 per month. "We were living hand to mouth and spent all that my father earned," says Singh.

"With my income, we hope to start saving." A big lacunae of the NSDC skills drive is that the institutes have not managed 100% placement. According to Tahsin Zahid, CEO of GRAS, it does 75% placement because students dropped out or were reluctant to relocate". "It's early days and the model is evolving," says Madhav Chavan, founder of Pratham. Chenoy adds the NSDC is working to see what can be done to ensure 100% placement—and change more lives like Teetu Singh's.

6 Nov, 2012, 10.40AM IST, John Samuel Raja D,ET Bureau

Agenda for reforms: 10 no-brainer policy changes that government can ring in today

http://economictimes.indiatimes.com/news/economy/policy/Agenda-for-reforms-10-no-brainer-policy-changes-that-government-can-ring-in-today/articleshow/17108380.cms2

inShare<a target="_blank" href="http://netspiderads2.indiatimes.com/ads.dll/clickthrough?slotid=37105"><img alt="Advertisement" height="71" width="640" border="0" src="http://netspiderads2.indiatimes.com/ads.dll/photoserv?slotid=37105"></a>

Agenda for reforms: 10 no-brainer policy changes that the government can ring in today.

BSE

167.35

0.40 (0.24%)

Vol:748628 shares traded

NSE

167.50

0.80 (0.48%)

Vol:410585 shares traded

Prices|Financials|Company Info|Reports

hey don't need Parliament approval. They are not political no-nos. ET outlines 10 obvious-and impactful-policy changes the government can push through easily today.

Full Coverage: ET Awards for Corporate Excellence 2012

1) Form a DFI Focused on Infrastructure

IIFCL was to play this role, but it has not picked up, says Vinayak Chatterjee, chairman of Feedback Ventures. Such a focussed development financial institution will play two key roles.

One, credit enhancement, where it extends a partial or full guarantee to infrastructure companies, helping them raise money easily at a lower interest rate.

Two, 'take out financing', where DFIs come in after seven years and roll over a company's debt to a new set of lenders. Alternatively, IIFCL could be reinvented to perform the above two functions.

Also Read: Will an ultra-cautious bureaucracy move the files despite policy push?

2) Bring SPV-Type Structure to Bid Out PPP Projects

The standard in a public-private project (PPP) is the government invites bid. The private player chosen has to obtain all statutory approvals and environmental clearances, throwing it into the cauldron of rent-seeking. This leads to two things. One, non-serious, but politically connected, players jump in.

Two, serious players expend time and money negotiating this landscape. A special purpose vehicle (SPV) for PPP projects, with all clearances in place, can reduce corruption and speed up projects.

3) Push Infrastructure PSUs to Spend their Cash Surpluses

According to Chatterjee, state-owned infrastructure companies have Rs 1,50,000 crore of cash that is not tied to any approved project. Most such companies are in sectors where the private sector is not allowed (like railways) or is allowed selectively (coal mining).

Or, they are dominant players (NTPC in power, GAILBSE -0.93 % in gas distribution and major ports). In almost all these areas, India is gasping for capacity as investments have fallen in the last four years.

* * |

4) Speed Up Road Construction

Road building, with its high multiplier effect, is one of the best ways to boost employment and income growth, says Govinda Rao, director of the National Institute of Public Finance and Policy.

But the highways construction programme is saddled with two problems: money stuck in arbitration and payment delays, and land acquisition. For example, the National Highways Authority of India (NHAI) has claims amounting to Rs 11,084 crore locked in disputes.

5) Clear Private Sector Dues by PSUs and Ministries

There's no official number on how much is due to the private sector from state-run companies and government departments— pending payments and disputes—but experts say it could be above Rs 1,00,000 crore.

So, that much less money is available to the private sector for investment. A way out could be to set up a quick dispute resolution mechanism within each sector.

12 Nov, 2012, 03.35AM IST, ET Bureau

ET Awards 2012: We'll push reforms to power economic growth, government tells India Inc

http://economictimes.indiatimes.com/news/news-by-company/corporate-trends/et-awards-2012-well-push-reforms-to-power-economic-growth-government-tells-india-inc/articleshow/17186746.cms0

inShare<a target="_blank" href="http://netspiderads2.indiatimes.com/ads.dll/clickthrough?slotid=37105"><img alt="Advertisement" height="71" width="640" border="0" src="http://netspiderads2.indiatimes.com/ads.dll/photoserv?slotid=37105"></a>

A panel comprising Commerce and Industry Minister Anand Sharma, Telecom Minister Kapil Sibal, Planning Commission Deputy Chairman Montek Singh Ahluwalia and UIDAI Chairman Nandan Nilekani faced over 400 business leaders on a crucial question: Can the recent burst of reforms return us to high growth?

EDITORS PICK

Last year, ET engaged government and business leaders with a 10-point 'Agenda for Renewal' to help arrest an alarming economic slowdown and kick start growth. This year, as Prime Minister Manmohan Singh reflected on the recent spurt of reforms, he used this agenda to measure his government's progress. "You will see that we have moved forward on most fronts in a substantive way. We have 'dispelled gloom & doom', improved the 'climate for foreign investment', improved 'ministry coordination', and are working hard to 'restore investor confi dence and the growth environment'. We have taken signifi cant steps in resolving 'energy & power' problems and tackling 'urbanisation' issues and improving the PDS," he said. That's progress, but more reforms are needed. A panel comprising Commerce and Industry Minister Anand Sharma, Telecom Minister Kapil Sibal, Planning Commission Deputy Chairman Montek Singh Ahluwalia and UIDAI Chairman Nandan Nilekani faced over 400 business leaders on a crucial question: Can the recent burst of reforms return us to high growth? Edited excerpts:

Deepak Parekh: India Inc is of the view that the worst is over. The wheels of government machinery have started moving and the recent announcement of reforms has given lot of confidence to the market. Now the question I want to ask is about corruption. Scams happen all over the world, all the time. People are fined heavily, organisations pay heavy fines, the legal machinery kicks in, but nothing comes to a standstill.

In India, when there is a scandal, decisions come to a standstill. It happened in telecom and in coal. Bureaucrats are wary of taking decisions for fear of being questioned afterwards or being harassed after they retire. How do we re-instil confidence amongst them? How do we find a better legal system where things move faster?

ET Awards 2012: Full Coverage I Highlights

Anand Sharma: Well, it is good that you have asked this question. The public discourse has become very shrill and the atmosphere has got vitiated. We must remember that we are a constitutional democracy, a rule-based and rule-governed society. There are due processes, but at the same time that must not deflect us from the larger objective of serving the supreme national interest of creating an environment where people believe in our country. Our global partners must trust us and we must continue on the same path on which we have embarked long back. India can ill afford an atmosphere of suspicion...of distrust.

We cannot allow this thing to fester where the civil servants don't take decisions for decades, and you have cases pending in the courts of law. We are still a country which is developing. We have the largest middle class perhaps in the developing world; at the same time we are also home to a large number of poor people. Now, what we gain from economic growth should be reinvested, redistributed for the common good.

If we do not have capital formation, if we do not have investments coming, if we do not have decisions being taken, if we have a situation where jobs are not being created, whose good is being served? Yes there are issues on which we need to collectively reflect as a nation where improvements are required, but you cannot change the Constitution. Let us believe in and respect the constitution of India. I agree with Deepak Parekh. Let us continue with our work, let us continue with decision-making, reassure the system that people who are working in the interest of the Republic of India shall get that protection. This is everyone's duty and of the political leadership.

Bodhisatva Ganguli: Mr Sibal, would you like to comment on this?

Kapil Sibal: Deepak has raised a very important point. Let me just try and answer it in two-three different ways. Let us take the telecom sector. When did the paralysis start? It started in 2010, not because of government but because of what happened in the court of law. 122 licences were cancelled. The moment that happened, we started to set things right; we have taken quick decision, firm decisions. The result of which is that we are in the process of an auction which will start on 12th of November.

We tried our best to take decisions in such a manner that everybody is dealt with fairly. We have dealt with the paralysis effectively and I can assure you that while we were taking these decisions, the bureaucracy was with us a 100%. They never faltered. We took bold decisions in the sector.

Take education. Where has the bureaucracy faltered in education? We have taken decision after decision, whether it is school education or higher education. I do not think that anybody can say that there has been a paralysis. The paralysis occurred because of three factors - one, the erudition of the CAG; two, the media; and three, the court. It is the symbiotic relationship between these three institutions that has resulted in a situation that we find difficult to deal with on a daily basis and yet this government continues to take decisions.

In the telecom sector, we have announced three policies which will take us forward in the next 20 years - the telecom policy, the IT policy and the electronics design manufacturing systems policy. Where is the paralysis? If there is any paralysis, it is because Parliament is not functioning. Is the government responsible for it? Maybe partly, but there is an equal responsibility on those who sit on the other side. Parliament is a forum for debate. If you cannot pass laws, then the perception is there is a paralysis. But the source of paralysis is not government, either in our executive decision-making or in the context of our participation in Parliament.

* * |

(Times Group MD Vineet Jain, Maharashtra chief minister Prithviraj Chavan, Prime Minister Manmohan Singh, Maharashtra governor K Sankaranarayanan and Union commerce and industry minister Anand Sharma put their minds together.)

No comments:

Post a Comment